Addressing the tax challenges arising from the digitalization of the global economy has become one of the top priorities for many countries and international organizations such as OECD and UN that contributed to creating a fair environment for ensuring taxation on a global scale. Conventional tax rules are no longer efficient to provide taxation of profits in the field of electronic commerce. Therefore, tax authorities are urged to harmonize their tax legislation with international standards to prevent the erosion of the tax base.

In this regard, Articles 33.8-1 and 169.8 were added to the local Tax Code, and the “Regulations for electronic tax registration, re-registration and de-registration of a non-resident carrying out electronic commerce through the Internet information resource” was approved by the decision of the Cabinet of Ministers of the Republic of Azerbaijan.

According to the abovementioned Regulations State Tax Service has already set up a platform to ensure tax administration for e-commerce activities on its online Internet Tax Office. Currently, the e-registration of non-residents carrying out e-commerce is available.

Article 33.8-1 of the national Tax Code stipulates that non-residents who receive income from works and services provided to persons not registered as taxpayer in the Republic of Azerbaijan, except those operating through a permanent representative office in the Republic of Azerbaijan, shall register electronically in the Republic of Azerbaijan.

The non-resident shall register by accessing https://ecommerce.e-taxes.gov.az/ website.

The ecommerce@taxes.gov.az e-mail address can used to receive support regarding e-registration procedures.

I. VAT on Digital Services

1. Who are non-residents providing digital services through e-commerce?

Cavab: Non-residents are persons who provide digital services via the internet.

Digital services include:

- provision of services and performance of works through internet information resources;

- supply or download of electronic books (e-books);

- supply or download of music;

- supply or download of audio and video materials;

- supply or download of graphic images;

- supply or download of virtual games;

- supply or download of software;

- placement, distribution, and management of advertisements;

- provision of other similar electronic services supplied in a digital environment.

2. To whom do non-residents engaged in e-commerce provide their digital services?

Answer: Non-residents engaged in e-commerce provide their goods and services via internet information resources to persons not registered with the tax authorities in the Republic of Azerbaijan, i.e. final consumers.

3. Do these rules apply to B2B (Business-to-Business) transactions?

Answer: No. These rules apply only to B2C (Business-to-Consumer) transactions. For B2B transactions, VAT liability is fulfilled by the local recipient under the reverse charge mechanism.

Non-residents may rely on the tax identification number or other business identification information provided by the customer to determine whether a transaction is B2B.

4. Which services are not considered digital services?

Answer: The following services are not considered services provided through e-commerce:

1. The following services provided via email or other interactive communication tools:

- consulting services;

- legal services;

- financial and accounting services;

- design and engineering services;

2. Educational and training services conducted in real time via the internet;

3. Online booking of tickets for science, education, cultural, sports and entertainment events.

5. Is there a turnover threshold for non-residents and when does it apply?

Answer: Yes. Non-residents providing digital services via internet information resources to individuals (consumers) located in the Republic of Azerbaijan are required to register for tax purposes if their annual turnover from such activities exceeds USD 10,000 (or its equivalent in AZN) within a calendar year. This threshold applies only to B2C transactions. Non-residents below this threshold may register voluntarily.

6. When does mandatory registration apply?

Answer: Mandatory VAT registration enters into force on 1 September 2026. Until that date, registration remains voluntary.

7. How is the customer’s location in Azerbaijan determined?

Answer: The customer’s location in Azerbaijan is determined based on the following indicators:

- the payment is made through a bank or payment service provider in the Republic of Azerbaijan;

- the IP address is associated with Azerbaijan;

- the mobile operator code (+994) is used;

- the residence or registration address is in the Republic of Azerbaijan.

8. What is the deadline for tax registration?

Answer: Non-residents are required to register electronically within 30 days after exceeding the threshold (USD 10,000). This requirement applies from 1 September 2026.

9. Who is not covered by these rules?

Answer: Non-residents operating through a permanent establishment in the Republic of Azerbaijan are not covered by these rules.

II. VAT Portal for Digital Services

1. How is tax registration of non-residents carried out?

Answer: Non-residents are registered electronically for VAT purposes through the platform established within the Internet Tax Office of the State Tax Service, and VAT returns are submitted via this platform.

2. What documents are required for registration?

Answer:

- registration (incorporation) or tax registration document in the country where the non-resident is registered;

- document confirming the appointment of a responsible person (decision, employment contract, etc.).

3. What information must be provided for registration?

Answer: Name of the non-resident, country of residence, legal and actual address, official website, email address, registration and tax identification document numbers, main business activity, payment currency, date of commencement of activities, and information on responsible persons (at least 2 individuals).

4. How long does the registration process take?

Answer: The tax authority reviews the submitted information and documents within 20 working days and completes the registration if no discrepancies are identified.

5. Why are bank details required from non-residents?

Answer: Bank details are required to ensure proper and effective VAT administration and to prevent double taxation for registered non-residents.

6. Are non-residents required to provide bank details during registration?

Answer: Yes. The following bank details must be provided:

- Acquirer – the bank or payment service provider processing the payment;

- MCC (Merchant Category Code) – a four-digit code identifying the type of business activity;

- Scheme – payment card network (e.g. Visa, MasterCard, etc.);

- Merchant ID – a unique identifier assigned to the merchant (15 digits);

- Acquirer ID – identification number of the acquiring institution;

- Acquirer Country – country where the acquirer is registered.

7. Can the selected currency be changed after registration?

Answer: No. Once selected, the currency cannot be changed.

8. In which cases may registration be rejected?

Answer: If prohibited activities are carried out, incorrect information is provided, or the established requirements are not met.

III. Submission of VAT Returns and Payment of VAT

1. How is the VAT return submitted?

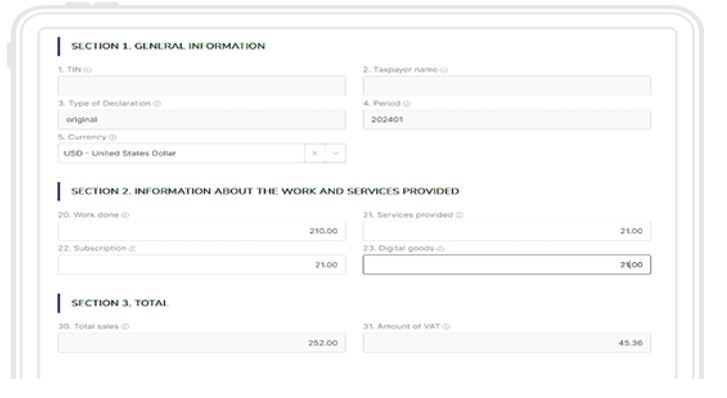

Answer: The VAT return is submitted electronically via the platform.

2. What period does the VAT reporting period cover?

Answer: The VAT reporting period is monthly.

3. When must the VAT return be submitted?

Answer: No later than the 20th day of the month following the reporting period.

4. Within what period must VAT be paid by registered non-residents?

Answer: Registered non-residents must pay VAT for each reporting period no later than the last day of the month following the reporting period.

5. What is the format of the VAT return?

Answer: The VAT return is designed in a simple and user-friendly format. It is submitted electronically based on minimal data requirements (total turnover and calculated VAT) to ensure that non-residents can easily and efficiently comply with their tax obligations.

6. What is the VAT rate?

Answer: The VAT rate is 18%.

7. In which currency can payments be made?

Answer: Payments can be made in the currency selected during registration:

- Azerbaijani manat (AZN)

- US dollar (USD)

- euro (EUR)

- pound sterling (GBP)

8. What are the main obligations of non-residents?

Answer:

- submit VAT returns on time and pay taxes;

- notify any changes in registration information within 20 working days;

- ensure the accuracy of submitted information.

9. Is it possible to resubmit an incorrectly filed return?

Answer: Yes. If an error or inconsistency is identified, an amended return for the relevant period may be resubmitted.

10. To which account should VAT be paid?

Answer: Detailed information on the account for tax payments in the Republic of Azerbaijan is available on the official website of the State Tax Service.

11. Who can be contacted for additional questions?

Answer: For questions and technical issues related to the use of the platform or registration, you may contact: ecommerce@taxes.gov.az